The Oklahoma plan for Group Hospital Services of Oklahoma opened its doors in the Tulsa Loan building at 4th and Main, March 15, 1940. The plan would soon adopt the Blue Cross name and logo. The interest in pre-paid hospital care had actually started in 1929 with a group of 1,500 school teachers in Dallas who contracted with Baylor Medical Center. These plans evolved as a result of the Great Depression.

In 1939, Oklahoma doctors went to Dallas to investigate this new form of paying for health care costs. The following year, Group Hospital Services of Oklahoma was born. The state headquarters was established in Tulsa since it was the first Oklahoma city to come up with $5,000 in seed money. By the end of 1949, Blue Cross of Oklahoma membership stood at 300,000 individuals and Blue Shield membership had reached over 169,000.

For more history of Blue Cross/Blue Shield, you are invited to listen to two former Blue Cross Chief Executive Officers, Ralph Rhoades and Ron King, on Voices of Oklahoma.com

Full Interview Transcript

Chapter 1 — 1:05 Introduction

Announcer: Group Hospital Services of Oklahoma known as the Oklahoma Plan opened its doors in the Tulsa Loan Building at 4th and Main on March 15th, 1940. The Plan would soon adopt the Blue Cross name and logo. The interest in prepaid hospital care had actually started in 1929, with a group of 1,500 school teachers in Dallas who contracted with Baylor Medical Center. These plans evolved as a result of the Depression.

In 1939, Oklahoma doctors went to Dallas to investigate this new form of paying for healthcare costs. The state headquarters was established in Tulsa since it was the first Oklahoma city to come up with $5,000 in seed money. By the end of 1949, Blue Cross of Oklahoma membership stood at three hundred thousand individuals and Blue Shield membership had reached over 169,000.

Now, you are invited to listen to two former Blue Cross Chief Executive Officers, Ralph Roads and Ron King, as they discuss the history and growth of Blue Cross Blue Shield on VoicesofOklahoma.com.

Chapter 2

Ron and Ralph – 3:50

John Erling: Today’s date is February 26, 2013. My name is John Erling and we are here today to tell the story of Blue Cross and Blue Shield, how the concept began, and how and why

Blue Cross Blue Shield

Two former Blue Cross CEOs discuss the healthcare leader’s history and growth.

it came to Oklahoma. Here to help tell the story are Ron King and Ralph Rhodes, former presidents of Blue Cross and Blue Shield of Oklahoma. Ralph, for our oral history record, would you please state your full name?

Ralph Short Rhodes: My full name Ralph Short Rhodes. Now, where did the Short come from?

It was my grandmother’s maiden name.

JE: Okay. And then your date of birth and present age.

RR: My date of birth is 11/27/26. I was born in a farmhouse in eastern Colorado. I’m eighty-six.

JE: Tell us where we’re recording this interview.

RR: Blue Cross and Blue Shield of Oklahoma’s head office.

JE: So you were born in Colorado, but let’s jump ahead. What was your first connection to Blue Cross and Blue Shield? When did that moment come about?

RR: I had a buddy, we went to TU, Tulsa University, I had a buddy who was working for Blue Cross and Blue Shield. I was doing a tryout at KTUL Radio and he called me one day and said, “I’m going to leave this organization I’m with, Blue Cross and Blue Shield, and you are the guy that I’ve picked to take my place. So that’s how I became for an interview, just out of the clear, blue sky because Jack Stewart said, “Go talk to him.” Which I did.

JE: What was the job?

RR: I’ll tell you what I did first, I used the addressograph machine to send out a newsletter.

JE: That was your first job?

RR: Yeah, that was the beginning of the Public Relations Department, which I then headed for fifteen years.

JE: You created the Public Relations Department?

RR: Yeah.

JE: That would have been in what year?

RR: 1950.

JE: So it was just on a whim? Somebody said, “I have picked you”?

RR: Yes. We had been schoolmates at Tulsa University.

JE: Right.

RR: It’s interesting about that guy who sent me to Blue Cross. They were then located in the basement of the Akdar Temple. Not many Tulsans remember the Akdar Temple, it’s a parking lot now. But in that basement we had probably about two or three hundred people. The Claims Department covered most of the floor space in that basement.

JE: We’re going to get into some of that. And also, of course, here is Ron King. So, Ron, would you state your full name and your date of birth and your present age?

Ronald Frank King: I’m Ronald Frank King, I was born February 14, 1948, so I’m now sixty-five.

JE: And where were you born?

RK: I was born in Bartlesville, Oklahoma.

JE: And raised then in that area?

RK: Raised in Bartlesville, yeah.

JE: What was your first connection to Blue Cross?

RK: I came to work at Blue Cross on May 18, 1980. At that time, Ralph, who was CEO, was searching for a Planning and Product Development department head. And I was at that time working for Bank of Oklahoma. It just so happened that the search firm that Ralph was using back in those days was Arthur Young and Company. And they were doing a search for somebody to come in in the Vice President position here at Blue Cross. And I was, coincidentally, working with them at Bank of Oklahoma on an audit. So the guy that was working with me at the bank was working with Ralph at Blue Cross on a separate assignment. Apparently they were going through a list of candidates and he just asked me one afternoon, he said, “Why don’t you put your name in the hat over at Blue Cross?” At that time I wasn’t really looking for a position, but I thought, “Why not?” And after a series of three or four interviews with Ralph I was hired as Vice President of Planning and Product Development.

JE: All right, so you guys have history, don’t you together?

RR: Yes we do.

RK: Yes.

JE: You can tell stories that we can’t even tell here, huh?

RK: Yes.

RR: Well, we can tell most of them.

JE: I’m sure you can.

Chapter 3

Home Office – 8:30

John Erling: So Blue Cross and Blue Shield, we will point out at the outset that they were developed separately with Blue Cross providing coverage for hospital services, and Blue Shield covered physician services. Let’s go back to the beginning. Its predecessor was developed by Justin Ford Kimball in 1929. Ralph, you perhaps can tell us that story.

Ralph Short Rhodes: Well, that came about as a result of the school district in Dallas, Texas. The teachers need a way for them to go to the hospital. Kimball then set up a program where they can pay so much a month into a fund and then they could go to a hospital

and have their babies or have their appendix out or whatever happened to teachers in those days in 1929.

JE: And we can point out, because we’ll be talking about costs as we go along here, the first plan guaranteed teachers twenty-one days of hospital care for six dollars a year.

RR: Yes.

Ronald Frank King: A year.

JE: Yeah.

RR: From there, however, Blue Cross started on the East Coast. It went from Dallas to Baltimore and Philadelphia up the East Coast and then ended up, you need to know this story, because N. D. Hellund was the first president in Oklahoma. N. D. Hellund is from Minnesota and Wisconsin. He called himself the Sweat Socks Salesman because he sold sweat socks to schools. But anyhow, that’s how the idea went from Dallas up the East Coast, then back into North Central, then came down to Oklahoma.

JE: And I understand there’s actually the Depression, 1929 and 1932 that drove some of these plans because people brought in chickens and meat to pay their bills.

RR: In those days, they paid their doctor bills with chickens and pork and a bushel of corn and so on.

JE: In my studies, similar plans actually went back to the 1600s, giving credit to a Montreal physician that far back.

RR: Yeah.

JE: But to bring it into modern times. The plan has been out there then for some time but it wasn’t in Oklahoma. So how did it come to Oklahoma?

RR: The Sisters of St. Anthony Hospital in Oklahoma City heard about this prepayment plan idea and they wanted to set something up in Oklahoma City. The sister who was in charge at that time was Sister Mary Agnes. She went to Philadelphia and Wisconsin and

Minnesota and got the idea that that was a pretty good idea. Then they were looking for who would set it up in Oklahoma. The Sweat Socks Salesman applied in a hotel room in Chicago. They liked him, I liked him, he was a likeable guy. Came to Tulsa. In order to get Tulsa involved the sisters put the headquarters over here instead of in Oklahoma City.

JE: There seems to be a story that leads up to that. Do you recall a Dr. James Stevenson?

RR: Dr. Jim Stevenson, yes.

JE: A Tulsa doctor, and Dr. Harry Turner led a carload of doctors in 1939 to investigate this thing of prepaid—

RR: Also, also.

JE: So then they spent about a year or so planning and gathering information.

RR: That is correct.

JE: That was then March 15, of 1940, Group Hospital Services of Oklahoma, the Oklahoma

Plan, as it was known then, opens its door and it happened to be at 4th and Main in the Tulsa Loan Building.

RR: Yes.

JE: That plan adopted the Blue Cross name and logo and— RR: Blue Shield came along later than the Blue Cross thing. RK: In ‘45, I think, is—

RR: Yes, 1945, there’s five year’s difference.

JE: Jump in any time here, now, Ron. You don’t have to wait until you become president of this.

RK: One of the interesting stories, I think, Ralph alluded to the St. Anthony sisters, and then there was a guy named Walter McBee that was involved, but he was kind of the first Director. And then, as Ralph said, N. D. Hellund was the first President of the plan. But it was an interesting story they used to tell about how it came about being in Tulsa versus Oklahoma City. Because both communities were interested in having a plan of this nature set up. There was a group of businessmen from both communities that went down to Dallas and looked at what was going on. They came back and decided that the first group of business guys that could raise the seed money, as they called it, for the plant, that’s where the home office would be. You’ll remember, John, the old Tulsa Club

downtown is where the Tulsa contingent met and they raised their five thousand dollars. They needed ten thousand dollars, is what they determined. They raised their five thousand dollars first, so that’s why really the plan was over here in Tulsa.

JE: Isn’t that amazing to this day?

RK: It was because they got together down at the Tulsa Club and decided, “Well, let’s do this, and here’s five thousand dollars to fund it.” That was really the launching pad for setting it up.

JE: Isn’t that interesting that E. K. Gaylord of Daily Oklahoman was an early investor in this program.

RK: He was.

JE: He was a major opponent of socialized medicine so he was early in.

RR: Yes.

RK: You know what is interesting, when you think about that being in 1939, 1940, and the thought of socialized medicine and here we are in 2013, now we’re talking about Obamacare being socialized medicine. And in between that is a fascinating history of healthcare and financing of healthcare.

JE: Very much so.

RK: It goes kind of full circle.

JE: Yeah. Then the first account was St. Anthony’s Hospital of Oklahoma City.

RK: Right. I think the first one in Tulsa was the Chamber of Commerce.

RR: That’s correct.

JE: Where for seventy-five cents a month or one dollar for a family of four you were eligible for thirty days of hospitalization.

RR: Yep.

RK: If I’m not mistaken, they’re still members.

JE: Oh really?

RK: Yeah, in fact, they offer a program for small business through the Tulsa Chamber. They’ve been with us all these years.

JE: Interesting some famous names that were on the board to begin with. T. C. Braniff, President of Braniff Airlines.

RK: Um-hmm (affirmative).

RR: Yes.

JE: Virgil Brown of Coca Cola Bottling, he became the Chair of the Board.

RR: Chairman of the Board.

JE: Yeah.

RR: That was before my time. I know looking at me you might say, “That was way before your time.” Just kidding.

RK: Another guy that was involved, which I found really interesting is my General Counsel when I became CEO was a lady named Jackie Haglund. Her husband, Dr. Roger Haglund, was on our Board of Directors. But her dad was one of the individuals at the Tulsa Club in 1940 that was instrumental in starting the plan. So you leapfrog from 1940 to when she became General Counsel in like 1997, fifty years there, and she winds up being a senior officer in the plans.

JE: That’s very interesting.

RK: Yeah.

JE: The Oklahoma Hospital Association and the Oklahoma State of Medical Association both supported the plan and they promoted it. So then, you bring up N. D. Hellund. He comes to Tulsa, December 5th, of 1941. Didn’t have insurance experience, did he?

RR: No insurance experience, as I said, he was a sweat socks salesman and used that all the time. He said, “Now, I may not know all I need to do know about hospitals and doctors but I can sure tell you about sweat socks.”

JE: That was his icebreaker, I’m sure, many times.

RR: Oh many times. He was the one who hired me so he did have pretty good judgment.

JE: Was he a tall man?

RR: No he was not a tall man, about my size, which is five foot nine. And was quite a guy.

JE: A salesman’s personality, obviously?

RR: Yes. Now the second president, which you’ll hear about, is Ralph Bethel. He was the accountant. Now Walter McBee, he reminds me of a movie star. He had long, blond hair and wore suede shoes. He later became President of the Texas Blue Cross and Blue Shield plan.

RK: I think an analogy with that, the eighth Plan President here—

JE: Who was it?

RK: A guy named Burt Marshall, who now is the Plan President in Texas. If you go back and look at the history books, Walter McBee, who was actually the first Senior Director, or whatever you want to call him, here in Oklahoma, went to Texas to run the Texas Plan in 1941 or—

RR: ‘40.

RK: Right. And now, in the year 2012, Burt Marshall went to Texas from the Oklahoma Plan to run the Texas Plan. So we’ve got to Oklahoma boys down in Texas running the Texas Plan.

Chapter 4

Pre-Paid Insurance – 2:15

John Erling: Back when Mr. Hellund was president, it was a pay before you go plan. It was not considered insurance.

Ralph Short Rhodes: True.

JE: Meaning what? Just explain the difference there.

RR: Well, it was a prepaid healthcare plan type. You prepaid ahead of time into our fund and when you needed care you went to the hospital. In those days, we didn’t even have an identification card, they handled everything by phone. It was quite a problem. We later got paper identification cards, and now plastic, of course. It was quite an organization, when I joined the plan I didn’t know what it was ‘cause I was fresh out of college and my father-in-law was the Chief of the Fire Department here in Tulsa, Vern Barton. I married his daughter. So I asked him, “What about this prepaid plan downtown?” He said, “What are you going to do? Go to work for them?” I said, “Yeah.” He said, “Go.” And so I went.

JE: Good advice.

RR: Yes. The firemen in Tulsa were very much behind the whole idea.

JE: They said petroleum, aviation industries, farmers, were a big block of enrollment back then. You’ve described what prepaid was. Then what was insurance?

RR: Well, insurance got to be scientific, that’s really what it was. If you were just a fund, you paid your money and you drew it out, or drew something out. Insurance, you were issued a contract and it became legal. If you paid your money in premiums you went to the hospital or the doctor and that was paid for you out of everybody’s premiums. It became less of a personal thing and more of a corporate thing.

JE: Okay.

Ronald Frank King: And that’s been debated for years ‘cause back then, and even today, people really don’t consider Blue Cross an insurance company, it’s a healthcare financing organization. The argument has been for years, like you can insure a boat or a house

you really can’t insure your health. That’s been debated for years and that’s why a lot of people say healthcare financing is what we do. We don’t really insure anything.

JE: And yo would agree with them?

RK: It’s a matter of semantics and I agree, right.

Chapter 5

War Years – 6:25

John Erling: December 7, 1941, Pearl Harbor comes along. Ralph, do you remember hearing about it?

Ralph Short Rhodes: Yes. I enlisted in the Air Force, that was before I came to Oklahoma.

JE: Right.

RR: I got out of the service in 1944, how I got here in Tulsa and met my bride and her father, I was on my way to Colorado, back to where I was born. I was going to enroll in Colorado College, which is a small college about the size of Tulsa University and Oklahoma City University, in Colorado Springs. I didn’t make it to Colorado Springs that time, but I met a blond-haired young lady and that’s how I stayed in Tulsa and went to Tulsa University. Eventually graduated and got married.

JE: So thank God for blonds, right?

RR: Yes. I haven’t left that.

JE: Right. Any comments about how the war years affected Blue Cross and Blue Shield?

RR: We just coasted really. They didn’t have an awful lot of marketing programs, as such, because people would hear about us and then they’d make a phone call or request somebody to come out, “What is this prepaid healthcare plan you’re talking about?” N.

D. Hellund and Walter McBee even hired school teachers to be their first marketing guys. That’s how we got into the schools in the early days.

JE: Lots of word of mouth then, wasn’t it?

RR: Yes.

JE: But there weren’t any other entities promoting prepaid at the time. There was no competition at the moment, was there?

RR: No there was no competition until after the war competition started showing up. I came home from Japan after McArthur took over over there and I was no longer in the Air Force and I was in the Infantry. Those changes happened kind of like Blue Cross when you’re in the battle of getting something started. It was kind of like a battle.

JE: Do you think one of the reasons Blue Cross Blue Shield is such a solid name today is because they had that early start, early on? Or maybe that washed away as competition came along?

RR: Well, it became a national organization rather speedily. They gave everybody the assignment of coming up with a logo and a slogan. A fellow in Minnesota, Van Steenwck, was kind of an artist and he sketched that out on his desk one day and submitted it to the other plans and they adopted it. And I forget at the moment how it came to be blue.

JE: Well, as I understand it, the blue came about when a Minnesota Hospital Administrator who was responsible for patient billing, he set aside those charges of those patients with coverage under this new prepaid concept. And then to indicate that those charges were covered he made with is pen, in blue ink, a blue cross on the billings to separate from those who didn’t have this kind of coverage. And so the artist, I’m speculating, perhaps took his inspiration for the cross from the administrator.

RR: You know, the hospitals were known for having a cross. That’s part of Van Steenwck used as his inspiration was a Christian cross.

JE: That changed over time.

RR: Over time we can become Blue Cross. We then went through a lot of effort and legal issues to become Blue Cross. We were sponsored at one time by the American Hospital Association. The Hospital Association spread it across the country. Oklahoma was among the first, however, to become a Blue Cross organization.

JE: Some of the cases that they were dealing with, illnesses in the ‘40s—

Ronald Frank King: Polio was the big one.

JE: Polio came on strong.

RR: Yeah. The guys that came home from World War II were primarily responsible for getting hospitals started and Blue Cross started, because all of us who were in that war were used to getting topnotch medical care in the service. So the veterans pretty much

lobbied Washington to say, “We need to have a healthcare program for our wives and our children.” The federal government then, right after World War II, expanded into encouraging it. Then in the late ‘40s Harry Truman, you know, was going to have a national health insurance plan. But the reason why they didn’t have a national health insurance plan at that time was because the senators all knew that there was a Blue Cross plan

in their state. And they used that as a justification for not having a national government program, because, “Let’s give them time to see if they can make it work.” Sure enough it did.

RK: Back then, you know, in the ‘40s and ‘50s, the proliferation of the Blue plans just exploded. At one time, I think, there’s like 120 different Blue plans, either a Cross or a Shield or a combined Cross and Shield throughout the United States. So a lot of states had two or three plans that operated that was so common that throughout the history of the Blues, as we call it, virtually, and still today, one in three Americans carry a Blue card. And there’s not too many organizations that can say that. In fact, back when I was a kid,

I remember people asking, “Well, who do you have your Blue Cross with?” When they were really asking, “Who do you have your health insurance with?” It got to be so prolific that people just looked at Blue Cross as a health insurer, you know, of choice.

JE: And I think that’s what I was alluding to earlier.

RK: Yeah.

JE: That’s what gave you your great start.

RK: In fact, they say, and I don’t know if this is really true but we like to brag about it, they claim that the Blue Cross and Blue Shield emblem is the second most recognized brand in the world, second to Coca Cola. Whether or not that’s true, I don’t know, but when you stop to think about one in three Americans carry that card, that’s pretty dynamic.

JE: Interesting, we were talking about illnesses back then in the ‘40s, cancer, only 11 out of 5,000 cases, and look how prevalent cancer is today.

RR: Yeah, cancer is now.

JE: What are we doing to ourselves?

RR: Well, we’re smoking and we’re drinking.

RK: And diet.

RR: And we’re eating badly. Lots of fat.

Chapter 6

Blue Cross – 6:10

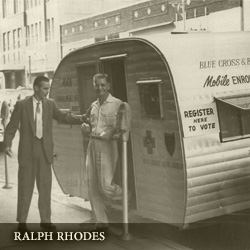

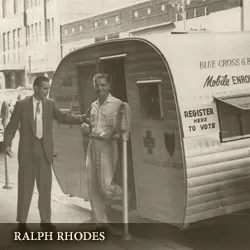

John Erling: By the end of 1944, Oklahoma City actually lagged the rest of the state in membership. Tulsa was the leading in enrollments.

Ronald Frank King: Of course, I wasn’t around, but I remember Ralph telling stories, they would go out and blanket the state. In fact, there was a picture in our history book of Ralph with a trailer. That’s really how they marketed the plan. They would go into a community, set up shop and do enrollment meetings there on Main Street. Put a banner up on Main Street. I think just the fact that Tulsa was the home office probably led to more enrollment being over here in the northeastern part of the state and then gradually working its way toward Oklahoma City and the Panhandle area.

JE: And that’s because there wasn’t any competition, they just assumed this is the way we’re going to insure our people, these plans.

RK: Right.

JE: And so you got a lot of free publicity.

Ralph Short Rhodes: Well, a lot of it we generated on our own. But it was free, no question about that. It had to come through the Tulsa Club is how that all occurred. The guys that put up the money all then enrolled their employees. Tulsa was first, so Oklahoma City was not as homogenous as Tulsa was in that regard.

JE: You’ve already addressed this, but the late ‘40s then was when the plan actually moved into the Akdar Shrine Building.

RR: Yes.

JE: I used to work for KRMG—

RR: Right above us.

JE: And I didn’t work there then, but they would talk about the live music on the second floor, I believe.

RR: Actually, it was the first floor.

JE: First floor.

RR: We were in the basement and KRMG was on the first floor.

JE: And they’d have these live western bands in there and you could hear that.

RR: We could hear it. My background, however, it originally was with KVOO, even before I got involved with KTUL.

JE: Now at KVOO what did you do?

RR: I was trying to be an announcer. It wasn’t very successful but that’s what I was trying to do.

JE: Were you around any of the Wells and those people?

RR: Well, I spent some time up there. When you’re going to school at TU they send you out into the community, which they did, and we went to KVOO to do back-to-college programs. Which it was back-to-college programs that I met Ben Henneke, who then became President of Tulsa University.

JE: I interviewed Dr. Henneke, those listening to this, you’ll be able to listen to him elsewhere on this website, who talks very much about back-to-college. It was his idea, actually.

RR: Yes it was his idea. I got acquainted with him in Joplin, Missouri, which is where I went to high school. He came up and did a back-to-college program up there. Because I asked a lot of questions of him at that program that they put on the for the high school, he made me promise that if I ever got to Tulsa I’d come by and see him. He was then in charge of the Speech and Theater Department at TU. That’s what brought me to Tulsa was to see Ben Henneke, before I went to Colorado. And he says, “Why don’t you just stay right here and go to school at TU?” And I did.

JE: Great choices, great people. Talking about all the free publicity you got on radio and TV, they just came out and promoted that. That would be something unheard of today, but they did that, for sure, because they thought—and they were doing a very good thing.

RR: Yes because the doctors and most of the local communities and the hospitals sponsored Blue Cross and Blue Shield. The doctors asked their pharmacists to cooperate and the pharmacy cooperated. So we had a built-in group of people who knew about Blue Cross and Blue Shield and they spread the word.

JE: The Blue Shield plan began as Oklahoma Physician Services?

RR: Yes.

JE: Which was a companion then to Blue Cross.

RR: In 1945, that was five years later after the Blue Cross plan came along.

JE: The Blue Shield, how did that come about?

RR: That came about because doctors in other parts of the country wanted to have a prepaid healthcare plan. So the doctors here, primarily in Tulsa, wanted a prepaid medical care plan. That’s how come the Blue Shield plan started here in Tulsa with Blue Cross.

JE: In 1954, the Oklahoma Blue Cross plan introduced extended benefits that covered the dreaded diseases, polio, scarlet fever, rabies, and that type of thing. By the end of that year, almost 250,000 Blue Cross members had enrolled in the extended benefits program. What was this doing to hospitals? Were they having to expand as this was happening?

RR: The thing that the federal government did was at the urging of the veterans that came back from World War II, the Hill Burton Funding Program to build hospital in communities was started. Incidentally, the first hospital in Oklahoma, the first hospital in the country too to get Hill Burton funds to build a hospital was in Nowata, Oklahoma. So the doctors

wanted to try out prepaid healthcare to see if it would work. And there were some forward-looking doctors who got behind it. And that’s why Blue Shield came into being, the Shield was later based on American Medical Association’s symbol.

JE: Rising costs, we’re talking about that today, this is when that started becoming an issue.

RK: Yeah, well, John, back when your question about Blue Shield and the physicians side, throughout history if you’ll look on the healthcare dollar, about sixty cents of every dollar is usually accounted for on the hospital side. There’s about 30 percent on the physician side, and then 10 percent on what we call the pharmacy and other medical expense. So that 30 percent got to starting to be a huge expense for people, and the hospital side was so successful with Cross that the doctors said, “Well, we need something similar to that because that big portion of the health dollar is getting to be really expensive.” And that’s what really generated the need for the Blue Shield side. But cost has always been an issue, and the rising cost has always been something that we’ve been addressing since day one. Probably always will.

Chapter 7

New Building – 2:25

John Erling: The ground was broken for a new three-story structure, 40,000 square feet an 12th and Boulder. In fact, they had the extra foundations to be poured so that eventually it would rise to twelve floors. So that was a big moment in the history of Blue Cross.

Ralph Short Rhodes: We had moved several times from the bank next door to the Bank of Oklahoma downtown, to the American Airlines Building, which is a parking lot now. Then to the Akdar Temple Building in the basement. And while we were in that basement, the executives of the Bank of Oklahoma said, “You’re going to have to have more space here shortly, aren’t you?” The basement of the Akdar Building was getting pretty full. N. D. Hellund said, “Why don’t we build a building somewhere or buy a building somewhere?” Well, the idea of building a building struck a note with people and our Board of Directors thought there was a movement of going towards the south end of downtown. But it

was the executives of the Bank of Oklahoma and the Board of Directors, doctors, and hospital people too, as well as business people, who said, “Let’s see what’s going on on South Boulder.” And that’s how we came to be in South Boulder.

JE: At that time, about the only building, I mean, was that considered getting far out?

RR: One of the first, yes. It was far out of downtown. But we were talking about a three-story

building at that time, the architects said, “All you need is a three-story building.” And N.

D. Hellund and Ralph Bethel and the rest of us said, “But some day we’re going go grow bigger than that. A three-story building, we might just as well prepare.” And that’s why we had the footings for a twelve-story building and nine stories were added at a later time.

JE: Were people noticing the growth of Blue Cross and Blue Shield so that they would be seeking you for employment?

RR: Well, it mainly came about because of the computers. They came along and we employed a large number of ladies who operated keyboards. They knew how to type and us guys didn’t know how to type very well. We hired a number of high school graduates who were experts typists and they became expert keyboard operators in the computer business.

Chapter 8

Oklahoma Health Status – 6:35

John Erling: We were talking about rising costs, but the indigent care was becoming a major concern about this time as well. And I don’t know how Blue Cross was addressing that or hospitals were.

Ronald Frank King: Oklahoma, unfortunately, has always been one of the top categories for having an uninsured population and an indigent population. In fact, back in the ‘90s when the Wellness programs and all the Stay Well programs and things like that were developed and implemented to try to improve the health of the state, it was a well- known fact that Oklahoma was the only state in the Union whose health status declined from year to year, based on national statistics. So we’ve had this problem ongoing for a long time. Back in those days, Post Trauma Syndrome wasn’t really known about for all the World War II veterans coming back. But all those guys that came back in the late ‘40s and ‘50s and ‘60s suffered from that tremendously. There’s been a lot of discussion about that, led to a lot of the indigent, the uninsured population. They didn’t know how to handle that type of disease. So you talk about the extended benefits, we really didn’t know what that was all about back in those days, like we do today. That was really the start of addressing the health status in the state of Oklahoma. And back in those days, being a rural state too, you didn’t have big urban centers that had big facilities to take care of people. They didn’t go to the doctor unless they absolutely had to. There’s a lot of factors that contributed to that, but that’s been a factor that we’ve been addressing for a long time. At one time, I remember when I first came on board back in the early

‘80s, Henry Bellmon came into the office and asked Ralph, he said, “We’ve got to do something.” He said, “This is such a serious issue, do something for me.” I remember going to meetings with Ralph and Henry Bellmon and he said, “Can you give me a twenty- dollar plan or something that we can sell to people to try to address this problem with the indigent population?” And we come up with a program. We joke and they called it El Cheapo back in those days, but we put together really a good benefit plan to take to the market. Bellmon got on the radio and TV with Ralph, we promoted this thing through the state. But quite candidly, as the old saying goes, the dogs didn’t like the dog food. They wouldn’t even buy a twenty-dollar product to insure themselves. So finding the magic solution to that is very difficult. And quite candidly, I don’t think anyone has yet.

JE: It’s being addressed today even, you don’t want to buy insurance.

RK: Yes.

JE: So that meeting with Henry Bellmon is a good idea, he certainly was sincere and you embraced it—

Ralph Short Rhodes: Well, I had met Henry because he became active in politics. I thought we ought to be participating in political affairs too. I went not a precinct meeting with the Executive Vice President of St. Johns Hospital here in Tulsa. Somehow or other I came out of that meeting elected Precinct Chairman. It was a railroad job, I think. Then I went looking in Oklahoma City for somebody that we could talk to that had political connections in Oklahoma City. J. T. Blankenship, who is a prominent family in Oklahoma City, at that same time was getting organized and we had a heck of a time finding the Republican headquarters. It was in an office building and it didn’t have a name on the door. Bellmon was doing the same thing. He was back from the war and he thought that the veterans ought to be a part of the political affairs because we needed some things.

Healthcare being one of them. So that’s how Blankenship and I both met Henry Bellmon. He later then became Chairman of the Republican party in Oklahoma, in a state that Republican was not a very popular word.

JE: That’s why you couldn’t find a Republican because it was all Democrat. And for those of you who will be listening years from now, here we are, it’s a very Republican state,

obviously. But it started with Henry Bellmon who shifted to Republicanism in Oklahoma. He was our first Republican governor, of course.

RR: Right. Very good friend of mine, incidentally, and he did a lot of things for me and my family, so he’s a joy.

JE: Well, we always knew him as matter of fact, down to earth, don’t mess around, straight shooting kind of a guy, and you would probably agree with that.

RR: Oh I would, 100 percent. When he ran for the US Senate I was going to Washington to pay a visit to Washington. He was there at the time. He thought I ought to spend

more time in Washington. And I did spend some time in Washington. But I had to leave Blue Cross in order to do that. But that was part of an experiment. In the process with

J. T. Blankenship and Henry Bellmon and myself, they wanted me to get involved as a candidate. N. D. Hellund was from Wisconsin-Minnesota area. He had been active in politics in that area. So Henry Bellmon and a group of the Tulsa Club people thought we would go to the Sun Ray Oil Company, who were enrolled in Blue Cross and Blue Shield, and they asked N. D. Hellund then if I could run for the state House of Representatives. We decided that it was a nice experiment to see if a corporate guy could get elected and serve in Oklahoma legislature. And I served in both the House of Representatives and the Senate in Oklahoma.

JE: While with Blue Cross and Blue Shield?

RR: While with Blue Cross and Blue Shield. To see if the experiment worked.

JE: And did it?

RR: No.

JE: Why not?

RR: Our fellow employees didn’t like for me to be proposing legislation that our customers didn’t necessarily agree with, was the main problem.

JE: Okay. So they heard feedback then on that then, obviously?

RR: They got feedback plenty, because I was a reformer and so was Henry Bellmon and so was J. T. Blankenship and folks like.

JE: But if this guy who works for Blue Cross is over there in the city proposing these things and we don’t like Blue Cross—

RR: That’s the idea, that’s the thing that occurred. And nobody ever asked me not to run, I just decided that I’d rather have a job at Blue Cross and Blue Shield than to be a politician.

JE: Right. Wise choice.

RR: Yes.

Chapter 9

Big Changers – 5:00

John Erling: In the ‘60s, there was a federal entry into the healthcare business, and then that promoted Blue Cross because the choice was Blue Cross Blue Shield.

Ronald Frank King: Yeah, there were two federal programs in the ‘60s that really changed

the landscape. One was the Federal Employee Program and the other was Medicare. And that was a springboard for a lot of changes in later years. But the Federal Employee Program was one of the programs that we have always been involved in since day

one. And Medicare as well. So those were the two big changes in the ‘60s that really impacted. And back then, health insurance, as we called it, or Blue Cross, was built around the group model. You’d market to the employers, they would bring their employees in. You’d set it up as a group account. And the Federal Employee Program become the largest group account in existence. And that’s significant when you leap forward now to 2000 plus when the market started shifting away from the group model that Ralph and these guys all put in and Blue Cross was built around. To now, a retail market or an individual market. Huge implications. But that was a major, major deal back in the ‘60s.

JE: Well, it just grew, Blue Cross enormously.

RK: Yeah.

JE: And fast. It must have been difficult to keep up with the growth of it at that point.

Ralph Short Rhodes: It was difficult. But we did in Oklahoma because of the situation among the farm population and other populations. We had what we called community enrollments. We enrolled groups of people in the community as individuals and made a

group out of the people in a certain city or county. That’s how we expanded in Oklahoma. And a number of states did the same thing, Texas being one of them.

JE: 1967, Ralph Bethel assumes the leadership of Blue Cross and Blue Shield from N. D. Hellund as you—

RR: Well, Ralph Bethel was primarily finance expert. He handled all the technical part of collecting money, lecturing all the rest of us, “You can’t spend more than you got.” And did a good job of it, incidentally. I explained to you that I went to Washington with Bellmon. I was up there, I’d had four years of Washington, DC, and I decided and my wife decided, it was time for me to come back to Oklahoma and she to come back to Oklahoma. I resigned from my job in Washington, got my suitcase unpacked, and on

a Saturday morning I got this phone call from Ralph Bethel who said, “Are you about through with all that glamorous stuff that you’ve been doing in Washington?” I said, “Yeah, I’m home.” He says, “I want to see you in my office Monday morning.” I said, “What do you got in mind?” He says, “Well, I think you might make a good president some day. Would you come see me Monday morning? We’ll talk about it.” That’s how I got well acquainted with Ralph Bethel.

JE: What was your job in Washington?

RR: In Washington I was with the Department of Commerce as an Economic Development Specialist.

JE: Did you enjoy that?

RR: Yes, but I’ll tell you, Bob Kerr was one of the guys that was really missed in Washington because he was from Oklahoma. He was famous among all the congressmen and senators.

JE: Probably the most powerful senator the state has ever had, the Senator Robert Kerr.

RR: Yes.

JE: Yeah.

RR: He was very nice to me too.

JE: Can you describe him and his personality? And how he’d come into a room and—

RR: He dominated a room, when he went in everybody turned and paid attention to Bob. John McClellan of Arkansas was one of Bob Kerr’s buddies. The Arkansas McClellan- Kerr Port out here is the result of those two guys trying to harness the Arkansas River.

JE: August of 1969, construction on the expanded nine-floor addition.

RR: Well, that was Ralph Bethel’s doing. Again, the issue was we had outgrown our space in the three stories and we might just as well plan on growing some more. So the nine-story addition was built because we had the beginnings of that already started.

JE: And in that period of time, updated their computer system, IBM 305 Ramac.

RR: Yeah. We were updating computer systems almost every year. And it was hard to find programmers. And the machines got bigger, now they’re smaller, but in those days the computer machines, just the machines occupied a whole floor. Then the programming staff got bigger and we had to provide room for them. Ralph Bethel was responsible for expanding that whole area. Did a good job.

Chapter 10

Blue Becomes One – 7:45

John Erling: We haven’t talked about the number of employees during your time. Do you recall how many employees you would have had?

Ralph Short Rhodes: When I retired we had twelve hundred, so we were building all the way from two hundred to twelve hundred over those twenty years that I was president. But they grew in technology. I think we grew pretty well. IBM was a big help to us and so was the Arthur Young Company.

JE: ‘73, then the two entities were merged into one corporation, Blue Cross and Blue Shield of Oklahoma. What did that do to the company?

RR: Well, it meant we had to redo all our literature. So the Public Relations and Advertising Department grew also.

Ronald Frank King: Before that time, there was actually a Shield organization and a Cross organization. And you would have floors that would be half Shield, half Cross. In fact, when I first went to work there in 1980, up on the 12th floor, which was the Executive Floor, there was a folding door that would actually divide the 12th floor in half. And I would, “I wonder why that is there?” And they told me the story that when they would have a board meeting they would pull that door and it would divide the floor and the Shield board would meet on one side of the wall and the Cross board would meet on the other side of the wall. So it was a very split organization, and when they combined that was a major improvement because they were then able to combine not only facilities but staffs. But it did lead to things like printing ID cards, and everything had to be reissued.

The computer systems had to be integrated. I can just imagine that was really just a big exercise to go through.

JE: Well, they competing against each other?

RR: No.

RK: No.

JE: It was just that they had a different product to sell, I guess.

RR: Well, the boards were in the same room and if they had only Blue Cross business they’d close the door and Blue Shield would have a cup of coffee. And it got to be awkward so we combined them into one. Then we decided along about there that we ought to do our own print shop. At our location there was a building that was next door to us, so we set up a print shop. Then we had to worry about paper, then we had to worry about staff that knew how to set up presses and get into printing.

JE: May 31st, 1977, you would secede Ralph Bethel as President and Chief Executive Officer.

Were you ready for the job? Were you nervous?

RR: Well, I came back in ‘72 to ‘77 and he was busy training me to become the president. Yes, I was ready for the job.

JE: What challenges did you face then as you took over?

RR: Well, of course, always there’s the business of money. Money was the big challenge in those days. I had had a lot of experience in the service with mathematics, codes, that sort of thing, so I hired the first actuary that the Blue system in Oklahoma had. I stole him from Mass Mutual in Boston.

JE: Tell us what then he brought to the table.

RR: He brought to the table a scientific way of relating illnesses to their cost and setting rates. I remember my first chore back when I joined Blue Cross and Blue Shield in 1950, my first chore was raising the rates from $2.65 a month to $4.65 a month. And everybody

asked me, “How did you get the two dollar increase?” Ralph Bethel figured it out on his abacas.

JE: Really?

RR: That’s absolutely correct. That’s how we got to that. Well, it stood us in good stead for quite a while, but we needed an actuary back then. We had consulting actuaries but we wanted one on our own staff that we could work with every month.

JE: In 1982, then, Blue Cross and Blue Shield implements the Staying Well Program for its employees. They were stressing the benefit of staying, obviously, physically fit and fitness classes, because you’d want people to be healthy. That was a program that your PR department had to promote?

RR: We had doctors that used to use our offices for the part-time practice and come treat our employees. So we decided that we needed a full time medical director. So we hired a full time medical director. He got acquainted with our full time actuary, then the programs got into quit smoking. I remember going to board meetings, the smoke-filled room. A couple of doctors were sitting next to me one time and they said, “Don’t you wish we could quit this?” I said, “Yeah, I’ve been smoking ever I since got into service in World War II. If you guys find out how to tell me how to quit smoking I’d appreciate it.”

As it turned out, they didn’t find out, I found it out myself because I had a pneumothorax. I busted a lung. I was standing lecturing to some employees, I went cough, I apparently

I had pneumonia and it caused blisters, you know, on your lungs, and one of the blisters broke. So that was the beginning of us talking about preventive medicine. How can we prevent people getting sick?

RK: And at the same time, tying back to your comments about cost, the groups at that time started coming forth saying, “Something has to be done. Cost is out of control.” It’s getting to be such a big issue on their balance sheet, healthcare cost as a group, that they were asking us, “Can’t we do something?” And that’s when the smoking cessation programs, diet programs, physical exercise groups would come forward and start paying for gym memberships and all kinds of things that we were trying, to improve the health status. Once again, one of the worst in the nation in Oklahoma, and trying to attempt to improve that.

JE: And we’re still trying to improve that.

RK: Still trying to improve that.

JE: In our day.

RR: I think we’re making some progress though because we’re talking now about prevention. How can we prevent illness? The antismoking business is not making as much progress as it used to but it ought to be making more. I don’t smoke anymore, thank God. Here I am, eighty-six.

JE: Well, it’s paid off because you’re looking well. And if Ron and I can look like you do at eighty-six we’ll be very pleased.

RR: Well, I quit drinking too. JE: Yeah? Well, so did I. RR: At the same time, so—

RK: One of the dynamics on the wellness side that I always found interesting, and looking back on it I didn’t really realize what we were doing. But when you leapfrog to the late ‘80s and early ‘90s we realized that, you know, the World War II generation, you’re not going to change their behavior and their habits. So let’s focus on the young people. In fact, Ralph, I think, was one of the first guys as CEO of a Blue plan to come forward in the early ‘90s and set up programs to start addressing, “How can we get into the schools? How can we start teaching young people wellness to try to improve this?” Knowing it’s not going to happen short-term, but long-term there’s going to be some benefits there.

We kind of went full circle with trying to address existing chronic illnesses and then trying to implement wellness programs, not just within groups, but into schools and into the young people. And we’re very active in that today, the plan is. Through their caring foundation for kids.

Chapter 11

Life Insurance – 4:05

John Erling: Then there was a feasibility study for life insurance that would come along. And the gentleman sitting right across from me here, Ron King, you were right in the middle of all that.

Ronald Frank King: I was, actually, when Ralph hired me in 1980, there was an individual named Rick McCutchin that worked for Ralph. When Ralph came up with the idea to come up with a life insurance company they actually set a company up with a blank tablet. He wanted to start from scratch. He said, “I want to do this right from the ground up and build it brick by brick.” And Rick was the guy that actually Ralph put in charge.

And then when he hired me in 1980, I only lasted about six months in my job and Ralph walked into my office. And I’ll never forget it, on a Friday afternoon, he said, “Monday I want you to go head up the life company.” I didn’t have any more idea than a rabbit about how to run a life insurance company, but that’s what Ralph wanted. He wanted somebody to go in, take this and built it, and learn, you know, as you do that. You ask Ralph about

Ralph Bethel training him, that was the real start of Ralph’s succession program with his senior guys. He had a rotation program. My first job in his rotation plan was running the member service life insurance company.

JE: I think we operated in the same building at the same time.

RK: Way it is—

JE: Because you were at Liberty Towers.

RK: Well, we actually were out on Broken Arrow Expressway in the Midway Building just for a short time, then we moved to Liberty Towers and that’s where your offices were.

JE: Then we were on the 23rd floor. So this began in a small apartment then really.

RK: Two apartments. We used bathtubs for file cabinets.

Ralph Short Rhodes: That’s right. We had people sitting in the kitchen using the counter for a desk.

RK: So it was really—

RR: They had their own refrigerator.

RK: It was a startup, ground-up operation, that’s how we built the company.

JE: But wasn’t there a call for one plan or one company to offer life? Because, I think, Blue Cross lost the CE Netco account because of that. They said, “Well, we want to deal with one company.” And so there was reason to begin to look at life insurance.

RK: That was really the initial start of what we call bundling. You hear bundling a lot today, well, back then the groups were saying, “Can we write one check for health and life?”

That really started the process. Really, the live insurance side was a key piece, but an equally large piece of that was the disability coverage, short-term and long-term

disability. It started coming into play back in the ‘70s and ‘80s and we had some pretty aggressive disability programs tied in with the life company.

JE: So as you said earlier, you really didn’t know much about this. You were on a real learning curve then, weren’t you?

RK: Real learning curve.

JE: Who were you learning from? Who were you reaching out to?

RK: There was an organization here in Tulsa called Southwest Insurance Organization, lot of life people belonged to that so we started networking with them. There were probably half a dozen Blue plans that started about the same time, and we had a life

organization. We’d all get together and meet, exchange ideas and products, but it was really just osmosis. We’d try to copy what we’d seen in the marketplace. We’d sit down with groups, “What do you want?” A national organization, Lincoln National Life, was a huge help to us. Right when I first went to work there as part of the planning operation, Ralph was really engaged at that point with an organization in Colorado, Rocky Mountain Life, who had started a program just previous to us starting ours. I remember the guy

running Rocky Mountain Life telling a story of how Ralph got on an airplane one week and came out there and come back there with a briefcase full of contracts and policies. And then he come back and said, “Here, I want you to take these and develop these for Oklahoma.” That was kind of our placard for developing programs and products. So the Colorado Blues and the Oklahoma Blues worked hand in hand for years on life products. It was a big help.

JE: And you saw this fine young man doing a good job, didn’t you?

RR: Yes I did find that out. He did a good job. He’s done a good job all the way through his career here.

FRK:Well, thank you, sir, that means a lot. Some days I wondered.

JE: I’m sure.

Chapter 12

HMO – PPO – 6:15

John Erling: There was a move then to HMOs, health maintenance organization

Ronald Frank King: Contract medicine.

JE: Yeah.

RK: Oh mercy.

JE: Why do you say it that way?

RK: When HMOs and PPOs first came about, back in the ‘80s, that was just almost communism. And the hospitals at that time really resisted because what came with that was price controls, with the hospitals. Back when Medicare came about there were any number of cost control measures implemented after Medicare trying to retain cost. And one of those was called DRGs, Diagnostic Related Groupings. And when we did contract medicine we incorporated in the HMO and PPO contracts with physicians and hospitals price controls and price groupings. For us to come forward as an insurance company or a financier to tell the hospitals and doctors, “This is what we’re going to pay you,” instead of them dictating to us what they were going to charge, it created some interesting meetings.

JE: That we can’t go into right here?

RK: No, we can. In fact, we wanted to do an HMO and a PPO but Ralph made a decision, “I don’t want to be the first in the marketplace.” Which looking back was a very wise decision. So we let Prudential come into the marketplace and watched them get beat

up royally by hospitals and docs and the media. ‘Cause nobody really understood what this was all about. But shortly after that, we decided we needed to enter into the PPO, the managed care realm, as they called it. Ralph called myself and another individual, Jack Walker, who was another senior officer in his office, and said, “Jack, you’re going to do the HMO. And, Ron, you’re going to do the PPO. So go figure out how we do this.” We started going out and holding meetings and Ralph told me on the PPO, he said, “Two things are a must: We’ve got to have St. Francis and we’re got to have St. Johns.” St. Johns being closer to downtown, that was my first stop. He said, “You need to go talk to St. Johns.” I went into the meeting, and at that time, Sister Terese Goschalk was the CEO, who I learned to respect and admire tremendously over the years. For those who know Sister Terese, you know, she was about maybe four foot ten but carried a big stick and ran a good hospital. I went over for the meeting and she was sitting at the head of

the table with her staff around the table. And I come in, started my presentation and got into about ten minutes of my presentation and she just interrupted me and said, “Mr.

King,” and wiggled her finger at me to come out into the hall. So I got up from the table and went out into the hall and she let me know in certain terms that the meeting was over. That they were not going to be a player in anything like a PPO. Now, shortly after that, we did manage to get them into our network and we were glad to have them. But we were thrown out of several doctors’ offices and several hospitals in those days. They were always polite but it was a tough sale.

JE: But you could probably understand why they were bucking it.

RK: Yep.

JE: So then St. Francis, was that a lot easier to bring them in?

RK: Not really. In fact, what was really interesting with St. Francis, the Blue board was dictated in those days by a set of statutes in Oklahoma. As a not for profit mutual organization, which was kind of an animal of its own, we had a set of bylaws and statutes that dictated. We had two hospitals and four physicians and then nine laymen on the board. So part of the CEO’s job, back in those days, Ralph’s job was to make sure we had good quality board representation. So recruiting doctors to the board and recruiting hospitals to the board was a very important piece of the job. And at that time, Ralph had recruited the head of St. Francis, a guy named Lloyd Verred was on our board. So it was really an interesting dynamic to sit in a board meeting and hear the discussion about,

“Well, what are these PPOs we read about? Are we going to do one of those?” the board asking Ralph and staff. So as we started studying this and implementing it Lloyd was really kind of in the middle of everything trying to figure out which direction he was going to take the hospital. At the same time, he was over here on the Blue Cross board. And he was having fun with it. He was quite a character. He was from Louisiana, called himself a

Ragin’ Cajun. He was an interesting guy, very smart, ran a good ship. When it got down to the final decision making it got down between Ralph and Lloyd about how we’re going to make this thing work between St. Francis and Blue Cross. And they were able to come to an agreement, one that we could live with. It really had some board intervention, at that point.

JE: But the agreements were the same between hospitals, whatever you did?

RK: Yeah, yep.

JE: Then other hospitals at the time, Hillcrest, would they have come on?

RK: Hillcrest. But in the marketplace, then especially, at St. Johns and St. Francis, they were kind of the hospital of choice, as one way of putting it. They were the big hospitals. The groups migrated more toward St. Francis and St. Johns as far as group enrollments. Not that Hillcrest wasn’t important, because they were, but Hillcrest in those days, especially, were looked at as the indigent hospital. And then the big hospitals in Oklahoma City, you know, were the St. Anthonys and the Baptist. We did Tulsa first and then we migrated over to the Oklahoma City area.

JE: For those who are interested in reading about a study of it, they should do that. But would you assess now as you look back on HMOs and these programs, is it working the way you saw it? And is it as effective?

RK: Well, in the HMO piece, the model that was built under is they called it capitation, to where we would cap a payment to a physician, for example, and say, “We’re going to pay you X amount to take care of this individual or group of individuals.” Looking back on that, yeah, I think it was very successful. It introduced some price controls and it got the doctors and the hospitals thinking about, “How can we better manage providers delivering healthcare? How can we provide healthcare for this dollar?” Instead of it

just being a free market and a blank check type medicine. So yeah, I think it was very successful.

Chapter 13

Carry the Card – 4:58

John Erling: In ‘86, Blue Cross Blue Shield began a brand building advertising program based on the ‘84 Blue Cross Blue Shield Association Carry, the carrying card campaign. Why was that important? Why did we have to carry the card?

Ralph Short Rhodes: Well, people were beginning to steal our cross and shield.

JE: Oh really?

RR: Yes. So we embarked on a nationwide program to protect the cross and shield.

Ronald Frank King: From some other Blue plans, no less.

RR: Yes.

RK: Unbranded competition, as we call it.

JE: How would that benefit them?

RR: They’d use our cross and shield and our reputation in order to sell, get in on our market. RK: A good example is, in the ‘80s we started seeing some fragmentation of the Blue system, fragmentation meaning plans competing within a state. Because we all have a license

area that we are licensed to sell in. Fortunately for Oklahoma, we own the license in all of Oklahoma, but some states like California would have the Shield plan license in Southern California and the Cross plan up in Northern California and they got to competing, but they couldn’t use the cross and shield. So what they did, they would come out with what they call a nonbranded product. They would go into a market, Unicare, for example, was a name that they used. We had Unicare come into Oklahoma. Well, Unicare was owned by Wellpoint, which was a Blue licensee. Well, they’d come into Oklahoma marketing Unicare and they’d go into a group meeting and they’d say, “We have a program, we have a network, we have a product that’s very competitive in the marketplace and it’s called Unicare.” “Well, who’s Unicare?” “Well, we can’t really say but it’s really Blue Cross and Blue Shield of California.” And that’s what the brokers were selling.

JE: Oh.

RK: “If you buy this you’re really getting Blue Cross value, you’re really getting Blue Cross service, it’s just called something different.” And that’s when the concept came up with carry the carrying card. And I know Ralph spent tons of time in Chicago in national board meetings trying to figure out, “How can we not go from state to state, but how can we have a Blue card that is carried from state to state to state, so people can get their healthcare through Blue Cross and Blue Shield?” If they’ve got an Oklahoma Blue Cross card they can go to Texas or New York and carry the carrying card and it be recognized as Blue Cross and Blue Shield—as one.

JE: Hmm.

RK: And that’s how that concept come about.

JE: Interesting. By the middle of the decade then in ‘85, the plan employed 699 employees, had outgrown its twelve-story building, and over Labor Day weekend in ‘85, about 110 employees moved to the Texaco Building at 15th and Boulder.

RR: Yes.

JE: So you’re spreading out?

RR: Well, not just the Texaco Building. We had another group that we bought a small building

for that moved into the one just this side of Texaco, Cowani Oil. We were growing so much and having to find space for the people that we had to start looking for where could we put people? We expanded into the Texaco Building, the Cowani Oil Company Building, and then later, we bought the building that you’re in right now.

RK: But that wasn’t the big change for me. In 1986, Ralph came into my office one afternoon and said, “I’ve decided we’re not prominent enough in Oklahoma City. We’ve got to do something in Oklahoma City. How would you like to live in Oklahoma City?” I said, “Well, I don’t know,” I said, “I’ve never thought about that.” But anyway, we bought a building in Oklahoma City, which was the old Leeway Motor Freight Building out on Hefner Parkway.

Ralph moved me and my family to Oklahoma City and I was the lone, first occupant in a four-story building for about three months. I sat in that building and started recruiting staff. That’s how we built the Oklahoma City office, and we’ve filled the building up,

eventually. We hired our own marketing team for Oklahoma City, we weren’t competing, we were just expanding our markets. Had a full staff over there eventually of people in Oklahoma City. And that become a very important office for the growth of the plans. We were growing over here but something had to happen on the western part of the state.

JE: So that grew fast, probably—

RK: It did.

JE: Since you hadn’t been over there.

RR: Oh yeah, it did.

RK: Initially we hired about 100 employees over there. We had a little marketing office over there for years, over on Classum. Our lobbyist was there and we had some marketing people over there, but we really expanded the operations over there. In fact, we set up the Property and Casualty Company in that office and did a lot of things different, just to expand our presence in Oklahoma.

JE: How long were you there?

RKF: I came back here in ‘90, so I was over there about four, four and a half years.

JE: Did Ralph come over to your office over there and stay?

RKF:Ralph actually had an office over there as well, he spent a lot of time there. He’d come over there one week and spend a couple of days, then I’d be over here the next week for a couple of days. So we burned up a lot of turnpike hours and a lot of time.

Chapter 14

Childhood Obesity – 4:20

John Erling: Now in this year, 2013, a pilot program was launched. And the program helps build a baseline for the state assessment of childhood obesity, which is such a big conversation today.

Ronald Frank King: It is, and we’re engaged in working with them as far as the childhood obesity. Childhood diabetes is just rampant. When you look at what’s happening in the schools now, they’re trying to improve their diet, trying to replace the soda pop and all the things that these kids are drinking. So it’s a concerted effort with several publics

in the state, that we’re very engaged in that trying to get this turned around. ‘Cause they’re telling us this is going to be a major, major issue if we don’t get this thing turned around in their childhood. Then as a adults, the early onset of diabetes is going to have a tremendous health impact.

JE: The Oklahoma Caring Foundation operates five caring vans now, two of which are based in Tulsa, two in Oklahoma City, one operated by the Chocktow Nation Health Services and based in Southeast Oklahoma.

RK: Everyone knows the state of Oklahoma has several Indian tribes with the Indian Health Service. We’re working with Indian Health Service, trying to get into the tribes. We’d like to be able to put a van with some of the other major tribes with our health programs, and we’re working toward doing that.

JE: This is a nonprofit organization, but all these immunizations, where is all the money coming from?

RK: Blue Cross basically funds that, in addition to having our own fundraisers. We have fundraisers throughout the year, contributions, grants. We have a grant-writing team, they’ll go out and write a grant and we’ll get grants from various entities to support this. Blue Cross provides all the administrative cost and everything as an in kind contribution. The Champions of Health Program is an offshoot of this, and once again, like I said, it was an attempt to recognize the good things that are happening in healthcare through the hospitals, through the different agencies. We have one event a year and we bring in speakers. Last year we had Magic Johnson come in and talk health related issues. We had Laura Bush come in the year before. So we bring in some prominent speakers to

address healthcare issues, but at the same time, we recognize, along with our partners, all the good programs in the state that are doing things like wellness programs, programs for the aging, the caring for the kids. And there’s any number of programs in the state that we recognize and they can submit names. I don’t know, we have like maybe two hundred people submit recommendations and we give like seven awards a year. We give them a

cash award for their program as well as recognition for that program. And it’s like I say, it’s just something to focus on the good things that are going on and trying to get people to focus on improving wellness and these programs and things throughout the state.

JE: It’s almost like now that if you’re not doing anything for yourself it’s not because you weren’t informed or educated. The country and the state and our city is talking about it so much, how can you not hear it?

RK: Yeah, and the resources are there. And that’s the attempt of this program is to put resources out there that people can take advantage of. And quite candidly, why some people don’t take advantage of it it’s hard to understand. That’s why we want to be proactive in this and trying to promote it. So we’ve done any number of programs to try to address this.

JE: It’s just the national conversation now.

RK: Yeah.

JE: It must have made you feel good to know that you are helping people and it wasn’t all about money here. I mean, you were effecting people’s lives.

RK: It did. And you have to understand what people don’t understand, we are at a mutual not for profit organization. Technically what that means from a legal aspect is our members are the owners of this company. We don’t have stockholders or shareholders. And we would tell people, “As president, I’m no more an owner of this company than you are.

Every member is an owner of this organization. As a mutual company.”

Ralph Short Rhodes: There are a lot of—

RK: And a—

RR: —mutual companies in America.

RK: Our dollars don’t go back to stockholders, they go to you, and that’s why we need to reinvest your premium dollars back to improving your health and providing as much healthcare for you as we can for your premium dollar. About nine cents of every dollar goes to administration, but about ninety to ninety-one cents of every dollar goes back to that member and their healthcare. And that’s why it’s incumbent on Blue Cross, and this is what we really believe in, that we promote as much health and wellness for our owners and the members as we can. And return every penny we can to them because they are the owner of this company.

Chapter 15

Management Succession – 4:12

John Erling: January 3rd, 1997, when you passed the baton to Ron, was this with a great sigh of relief? Were you happy? Here it is, I’m out of here? What were your feelings at the time?

Ralph Short Rhodes: Oh, well, I signed on for five more years before that. I could have retired at sixty-five and I stayed till seventy. I love this organization, I love the people, I hopefully did a bunch to build it to the size it is today.

Ronald Frank King: I would wholeheartedly support that and he did. In fact, I mentioned his succession plan was an interesting program. And I got asked about it throughout my career. Because it had become very well-known in the Blue community. Ralph had four senior guys, at that time, senior vice presidents, and he literally would walk into your office on a Friday afternoon and he’d say, “Monday morning you’re going to be a Chief Financial Officer.” And myself, as an example, I’m a marketing major, I’m not a CPA. He would come in and say, “Monday you’re going to be a CFO.” And, I mean, that was it,

Monday morning you were the CFO of a billion dollar corporation. And it was really an interesting concept from the fact that by the time it was over and done with Ralph’s retirement, I was real fortunate in that I literally sat in every chair in the organization. I

was CFO, I was Chief Marketing guy, I was Chief Operations guy, I got to sit in all those chairs and run those divisions. It was a great learning experience, but at the same time, what we realized later was Ralph was giving the board a choice of four people that really knew how this organization was run. I don’t know if he would admit it or not, but that

was part of the five-year extension. He wasn’t through with his rotation and he wanted to make sure that he had the four guys through the rotation so that he could walk away and hand the board somebody that was really qualified, from an experienced point of view, anyway, to run the company.

JE: How long were you in each position as you rotated?

RK: It depended, usually about two to three.

JE: Oh really?

RK: Yeah. Looking back on that I often tell people—

RR: We shot for three, three was the magic.

RK: Yeah. You’d go in as CFO, for example, well, you’d have to bring all your staff in and they all knew he didn’t know come here from sic ‘em about being CFO. In fact, Ralph always had a saying, “I’ll give you a year to learn and a year to perform.” That was kind of how he ran the rotation. And it pretty much happened that way. It took us about a year to really get comfortable with knowing things. But as that rotation and management succession happened we got, of course, to watching one another and working with one another

because we knew my stop is going to be your seat. So I learned as much as I can working with staff and staff meetings and things about what was going on. It took about twelve to fifteen years to really get through that rotation plan.

JE: Wow. Where did you come up with that idea?

RR: I borrowed that from General Electric.

JE: Really?

RR: Yes.

RK: And it really, at times it got a little bit humorous, at times it got a lot frustrating, because people would realize, people being staff members, managers, vice presidents, that I could work with this guy in the next rotation. So everybody was a little bit standoffish sometimes and real careful not to burn bridges with people. It created a very interesting atmosphere.

JE: He says here he’s got a very nice smile and he’s very—

RK: Oh we got a kick out of it. I mean, he wasn’t stern, he’d come in with a big old grin on his face and you knew it was time. I mean, and we got to where we could pretty much

gauge, “Well, it’s about time.” It seemed like it was always on a Friday afternoon because he would come waltzing in and he’d have that kind of smirk on his face, and he’d say, “Monday.” And it was that quick.

JE: Did you emulate somebody as a leader in another company? Or did you draw from other people that might have influenced you?

RR: I was a student of General Electric, that’s where I borrowed that whole idea from. But I studied a lot of companies, not just General Electric.

Chapter 16

Obamacare – 5:32

John Erling: A little bit about the future here. Right now, currently in 2013, we have the Affordable Care Act, Obamacare, as it’s been called, using the President’s own words. He says, “Today the a hundred and five million people have seen a lifetime cap on their coverage lifted. So your patients no longer face the tragedy of approaching a lifetime limit in the middle of a round of chemotherapy.” What is your assessment of the Affordable Care Act? Is it something that should definitely be implemented at all levels?

Ronald Frank King: There’s so much unknown at this point because is the fact that the regulations for the Act have not even been really written, let alone passed. So there’s

so much unknown with that. But what we have seen is a major shift away, as I said earlier, from the group market to an individual market. Which is a huge change in the

insurance world. One of the factors that led to our merger in 2005, with the Illinois-Texas- New Mexico plans, Oklahoma merger, massive dollars, but to be able to manage that environment and to set up the programs that they’re talking about is going to be a major landscape change. But I have said for years, I’m still 100 percent convinced of this, I’ve always believed that somewhere in the Beltway of Washington, DC, there’s a little red brick building. And in that red brick building there is a diagram on a wall of how we get

to socialized medicine. And this is a huge step toward that. This is the first step, I think, toward really going to socialized medicine. And one of the factors key to that is what we’ve talked about with the federal employee program. When you look at the fact that the federal employee program is now the largest group program in the United States. It would be real easy for the federal government to come in and say, “Well, we’ll just use that as a model and we’ll just start folding people into the federal employee program.” And you’re in socialized medicine. Now, saying that, when will that happen? Who knows? It could be fifty years from now, but that’s where I see this headed. This is just one step toward a single-payer socialized type medicine with the government in control of that.

Now, will there be a role for the Blue plans? You bet. I think there always will be. And that’s why this shift in the marketplace is really critical right now and why so many of the Blue plans are looking at merger into one bigger plan. In fact, if you’ll look at the Blue system, when I came on board in 1980, there was a 117 Blue Cross Blue Shield licensees. Today there’s 38. So the consolidation is rampant and they’re doing that so that they’ll have the infrastructure with which to go out here and address this bigger marketplace. So I think from some aspects it’s brought some good things to the table, when you look at being able to cross state lines and portability it’s going to bring some things to the table with automating medical records and things of that nature that needs to happen. So there are some good things to it, but we really, I don’t think, understand the real impact this is going to have.

JE: E. K. Gaylord was spinning in his grave when you were just now talking about socialized—

RK: Yes he was.

JE: Finally then, capturing a point in time, because generations will listen back here, we have a special report from Time Magazine, and it’s why medical bills are killing us. It’s the first time the magazine has devoted one topic to their entire magazine.

RK: Well, John, there’s a really interesting phenomena in the health business. I used to have a little presentation I would give on health economics. I’d tell people, “You can forget everything you were talk in school on economics and supply and demand when you look at healthcare.” Because in the real world, when there’s a demand for something,